Oops! We couldn’t find any results...

Oops! We couldn’t find any results...

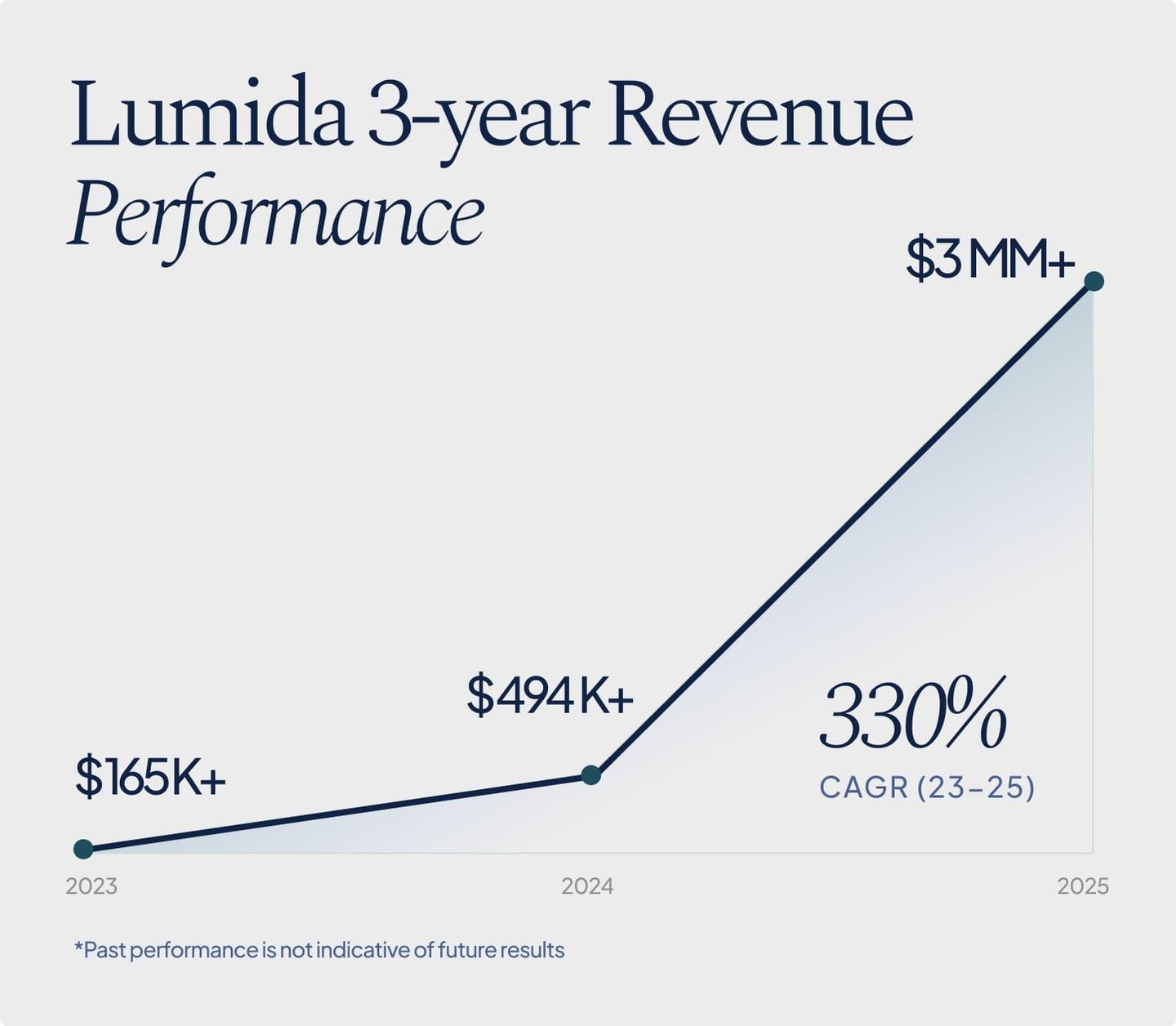

*Past performance is not indicative of future results

Opportunity

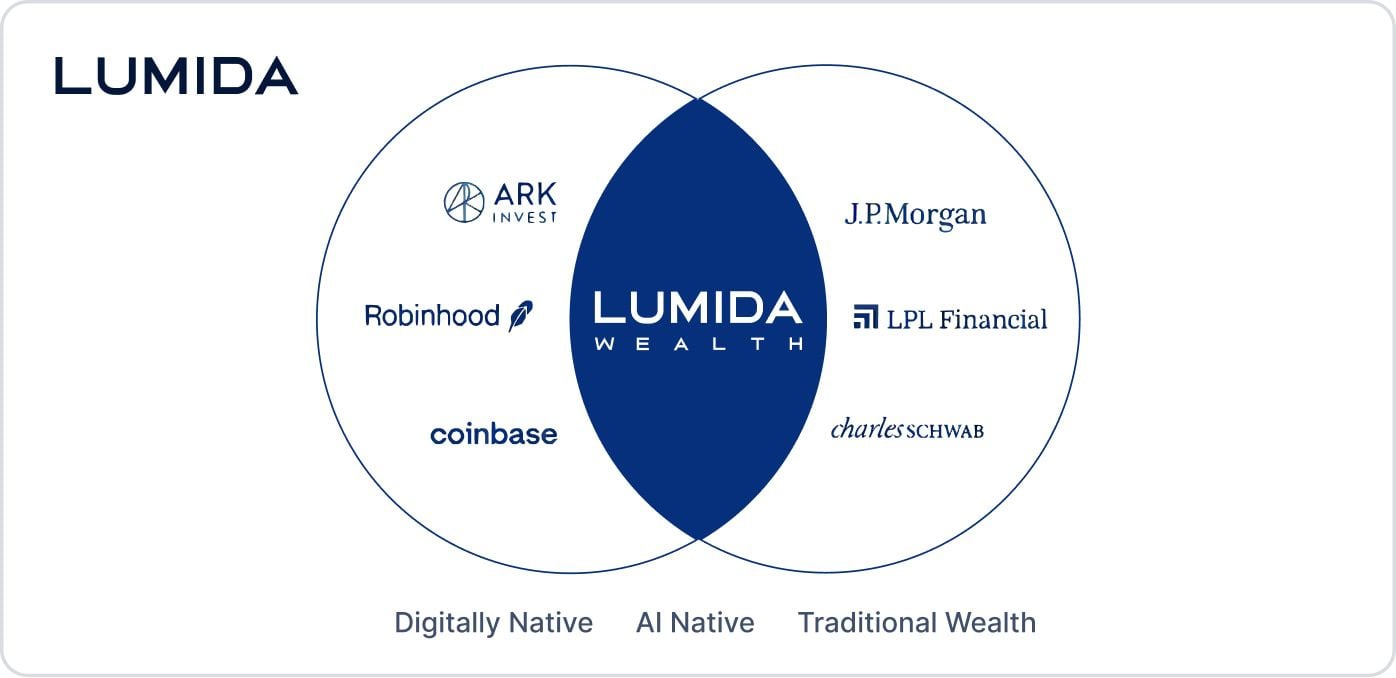

AI Will Eat Wealth Management

Every generation, a new technology disrupts an entire industry.

The computer. The internet. Now AI.

Lumida is building the future of wealth management. We believe AI native wealth managers will outperform traditional firms with 1/100th the headcount.

Meanwhile, $84 trillion in wealth is transferring to a generation that lives online. They don't watch CNBC. They don't want the US Open with a banker. They get news on TikTok, learn on YouTube, and want investing in the palm of their hand.

Old-school wealth managers haven't adapted. They're losing this generation by default.

Lumida is built for the AI Generation.

Traction

Our Traction Is Strong

2025 was a huge year for Lumida. Revenue up, traction accelerating.

Lumida has completed the hardest part. The "Zero to One" journey. In less than three years, we've built a brand, a community, and a track record.

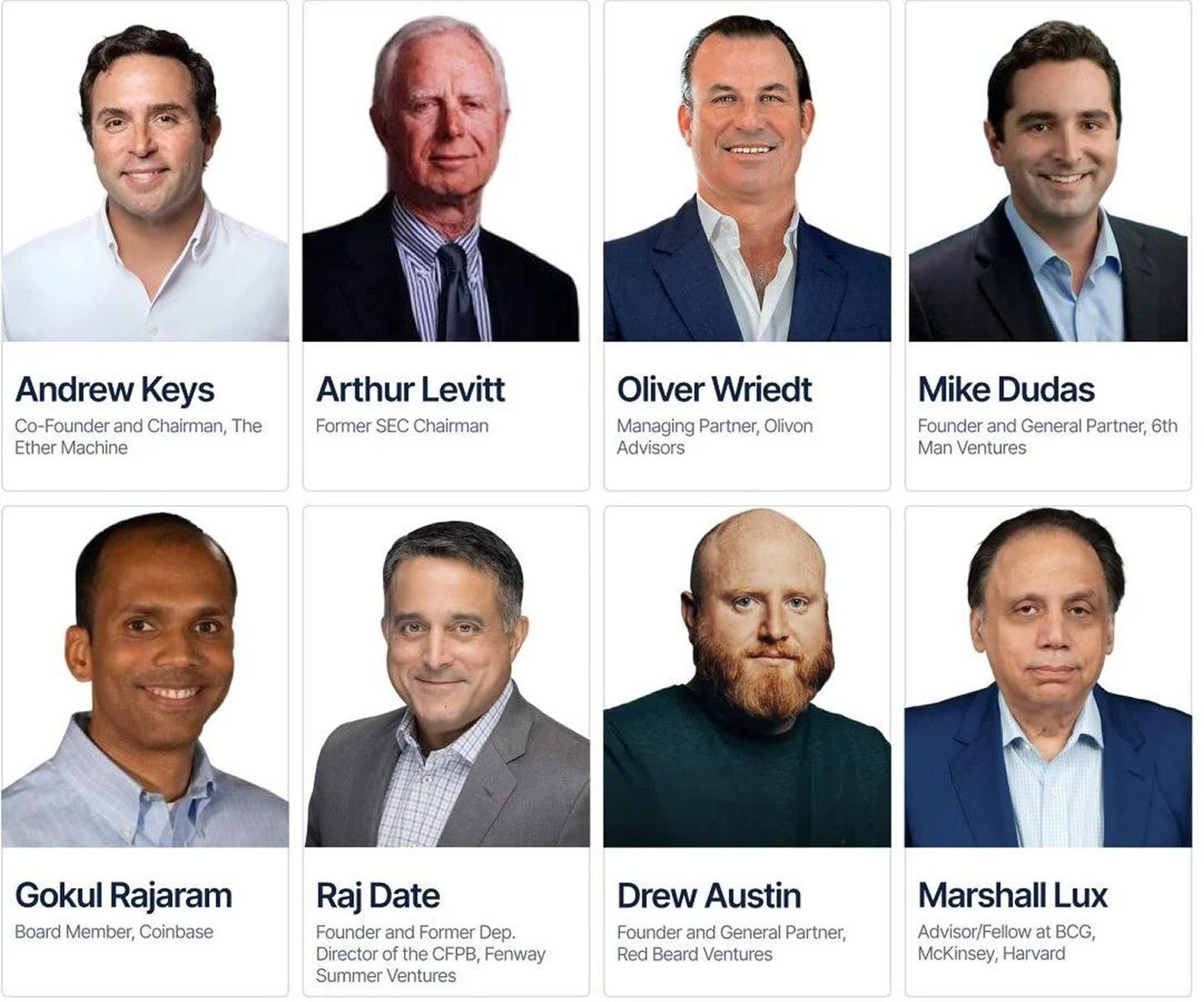

Investors

We Have World Class Investors

Lumida is backed by investors with board level experience at Circle, Coinbase, and SoFi before they went public.

Recognition

Lumida Recognition

Lumida is a regular voice on the podcasts investors listen to. Lumida's thought leadership has been published in the WSJ and American Banker.

Community

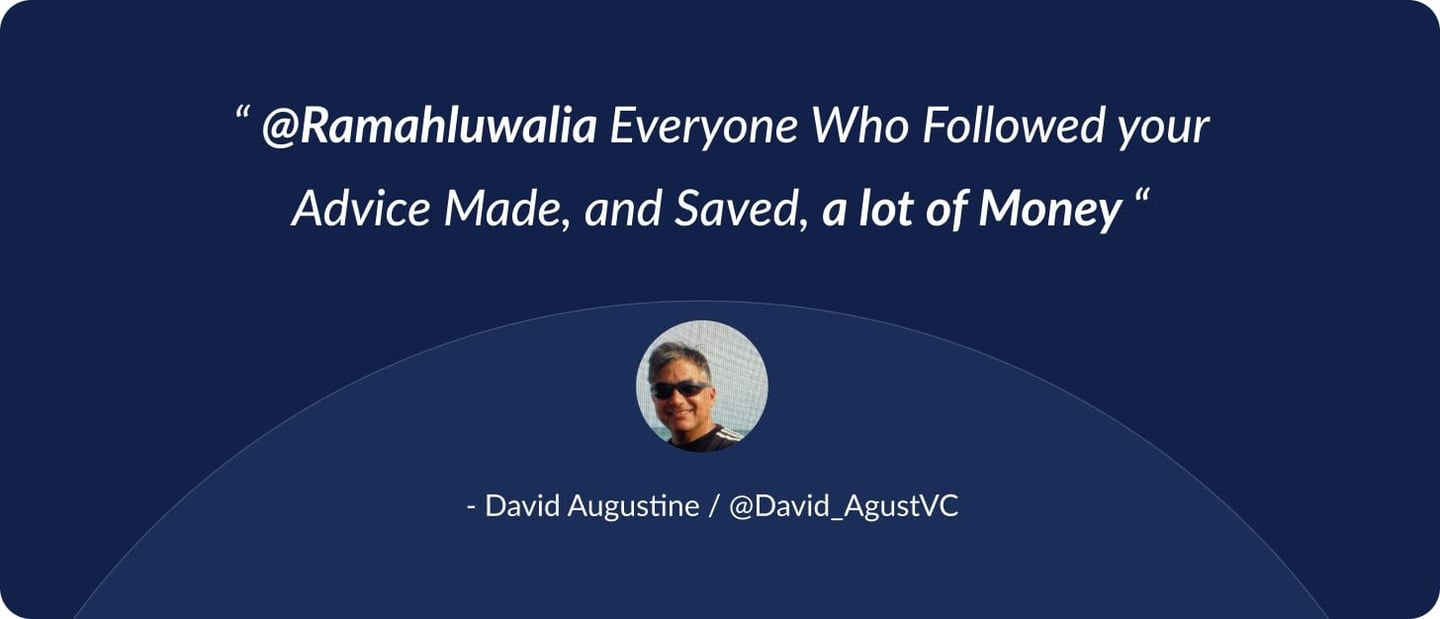

What People Say About Lumida

Don't take our word for it. Here's what investors are saying:

Individuals providing testimonials have not been compensated for their statements

Lumida Invest

Lumida Invest: Trade Smarter. Build Wealth.

Robinhood made trading accessible. Lumida makes it intelligent.

Today, Lumida Invest gives every user AI-powered analysis on every trade. The kind of intelligence that used to require a Goldman wealth desk.

But trading is just the start. Lumida is built for the full investor lifecycle: trades, long-term portfolios, tax strategy, and wealth-building.

Next: AI advisors that handle the work your human advisor charges 1% for.

Here's what that looks like:

Identify emerging themes and market shifts before the crowd does

Your AI analyst - always on, always ahead

Track the moves of Warren Buffett and leading hedge fund managers

AI confirms your instincts with clear buy and sell signals.

AI Advisor

Lumida is building the AI Advisor for the AI generation

Wealth management hasn't changed in 50 years. You pay 1% to a human advisor who reviews your portfolio quarterly and refers you out for everything else.

Lumida Invest changes the model entirely. An AI agent that knows your full financial picture and can guide you.

Available 24/7, at a fraction of the cost.

Your AI agent suggests what to buy or sell, harvests losses, and minimizes capital gains.

That's what we're building next. And people who got early access can't stop talking about it:

*The individuals providing testimonials have not been compensated for their statements.

Business Model

How Lumida Compounds

The Lumida Flywheel

Most wealth managers offer services. Lumida is a Wealth Architect - a self-reinforcing flywheel with AI at the center, designing every piece of your financial life into a single system.

- The Lumida Invest app brings users in.

- Our content earns their attention.

- The Tribe turns them into a community.

- Our community got CoreWeave before its IPO through Lumida Ventures.

- Lumida Wealth manages it for the long term.

- A future Lumida ETF will open access to every investor.

Every piece reinforces the next. AI compounds every turn.

Every Lumida investor is also a Lumida ambassador. Owners become users. Users become owners.

The conversation about Lumida happens at kitchen tables, in group chats, and across social feeds - by people who have a stake in our success.

That's the SoFi and Tesla playbook. Community as the growth engine, with ownership as the accelerant.

Our vision is to grow exponentially, and set the stage for a potential public market exit down the road.

The flywheel is built. The AI platform makes it spin faster. Our community makes sure it never stops.

*The individuals providing testimonials have not been compensated for their statements.